Finally, again let’s begin our analysis of strategic options for major actors in Auction 73, 700 MHz Band, with a look at the footprints established by many of those actors in two previous Lower 700 MHz auctions (Auction 44 and 49) and the AWS-1 auction (Auction 66):

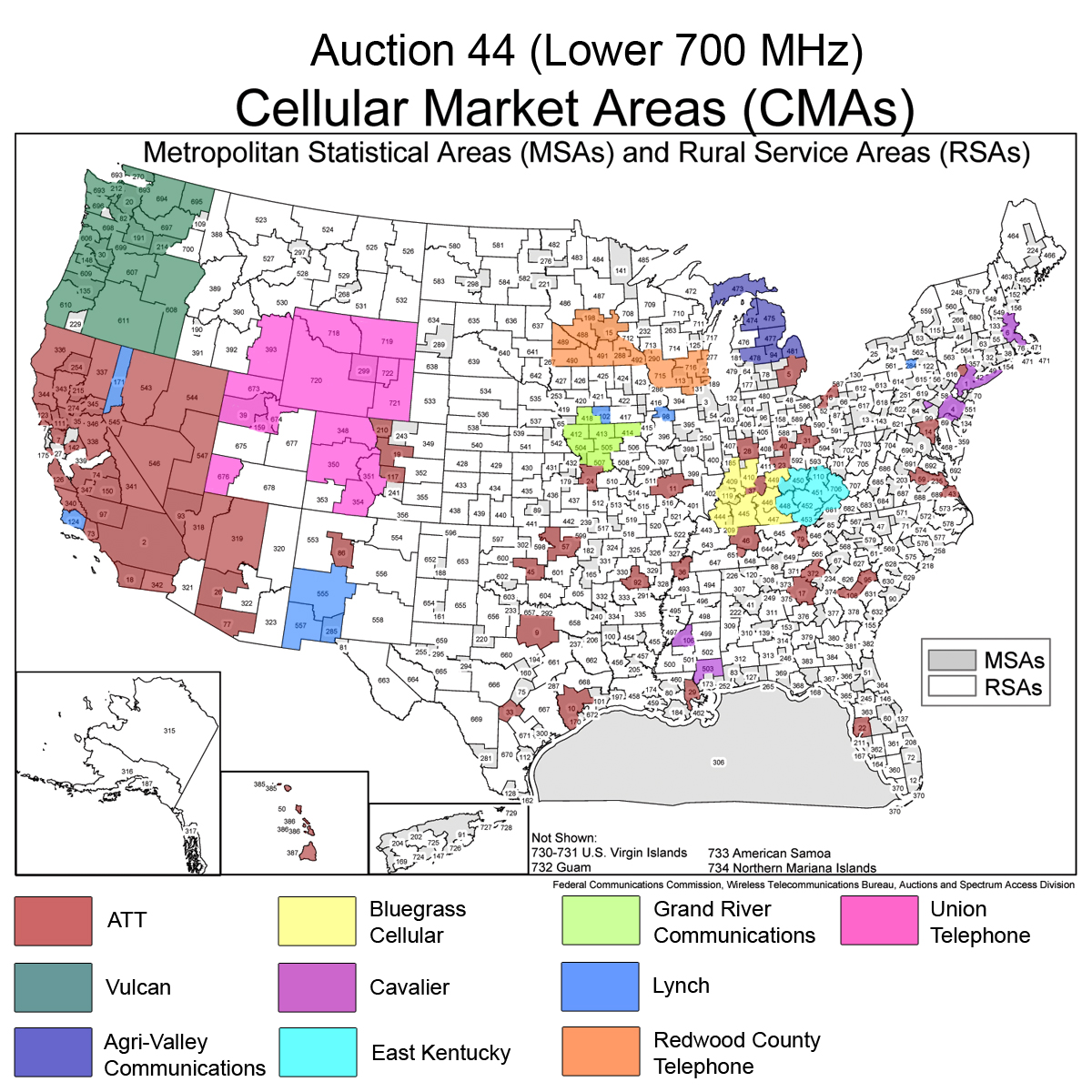

Cellular Market Areas (CMA) Map for Auction 44

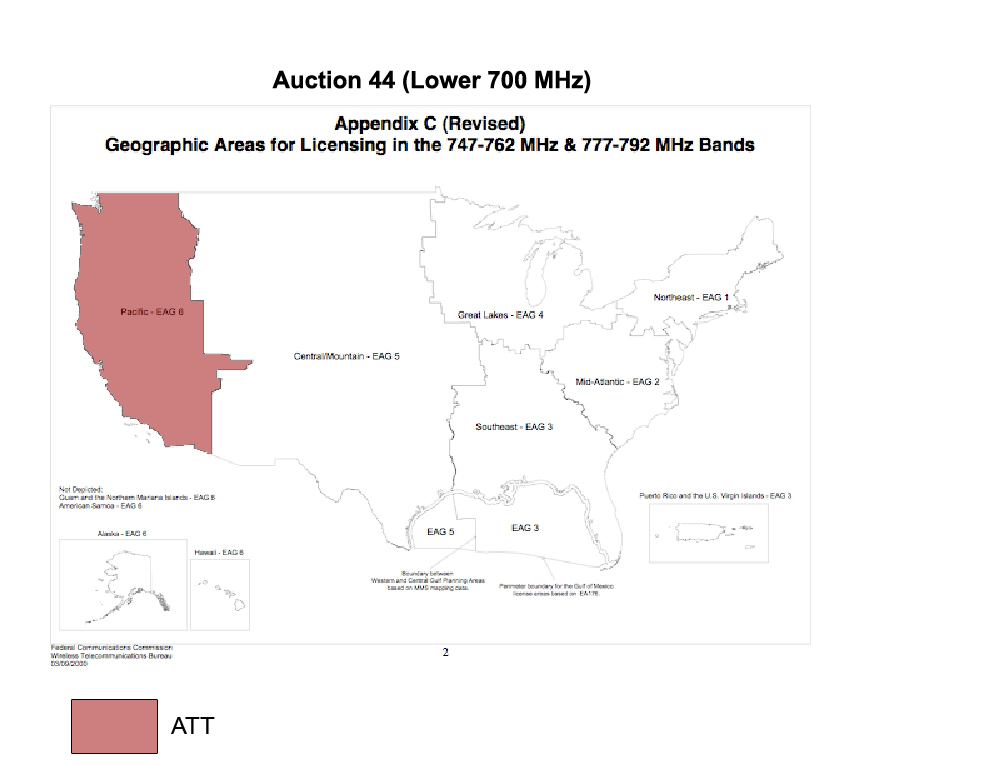

Economic Area Groupings (EAG) Map for Auction 44

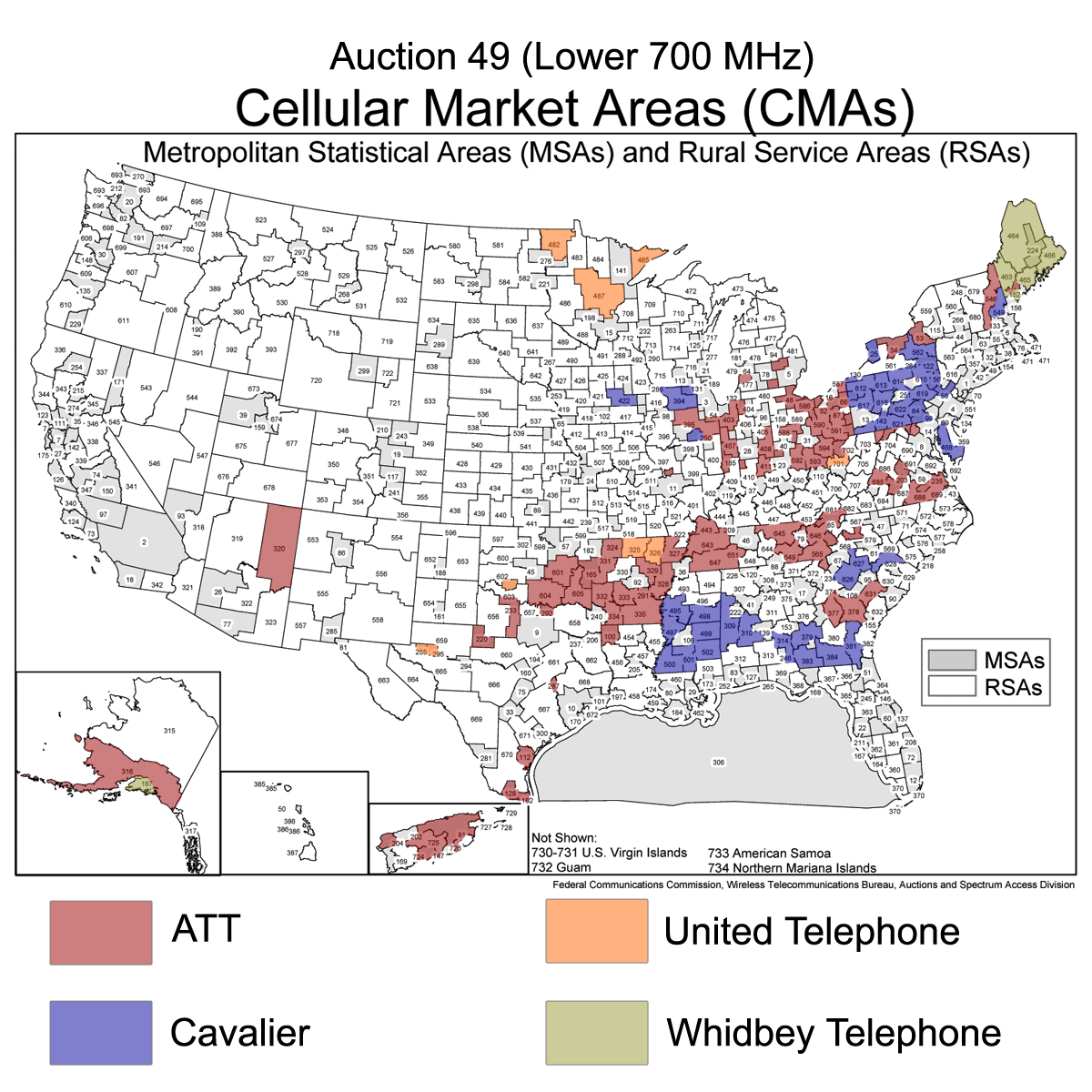

Cellular Market Areas (CMA) Map for Auction 49

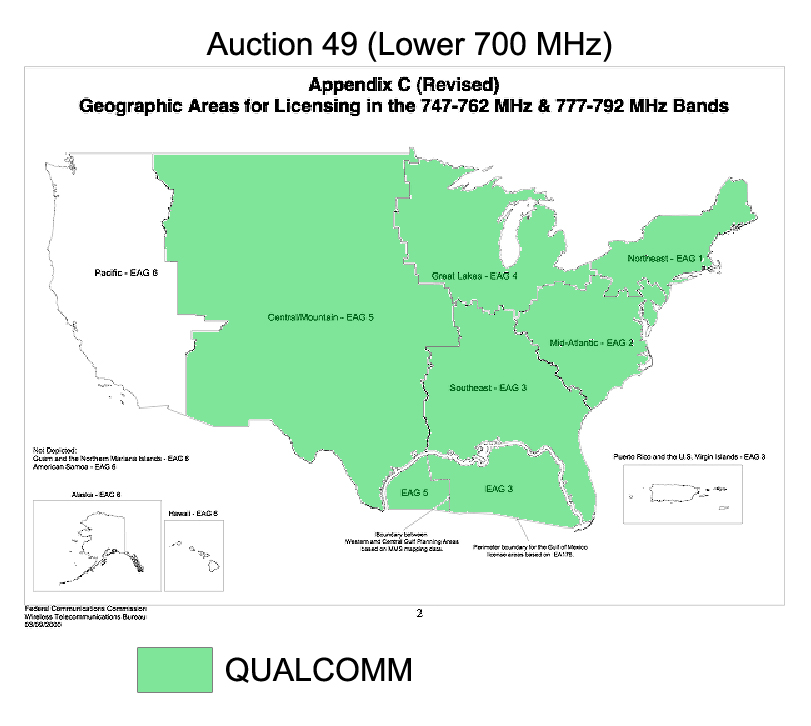

Economic Area Groupings (EAG) Map for Auction 49

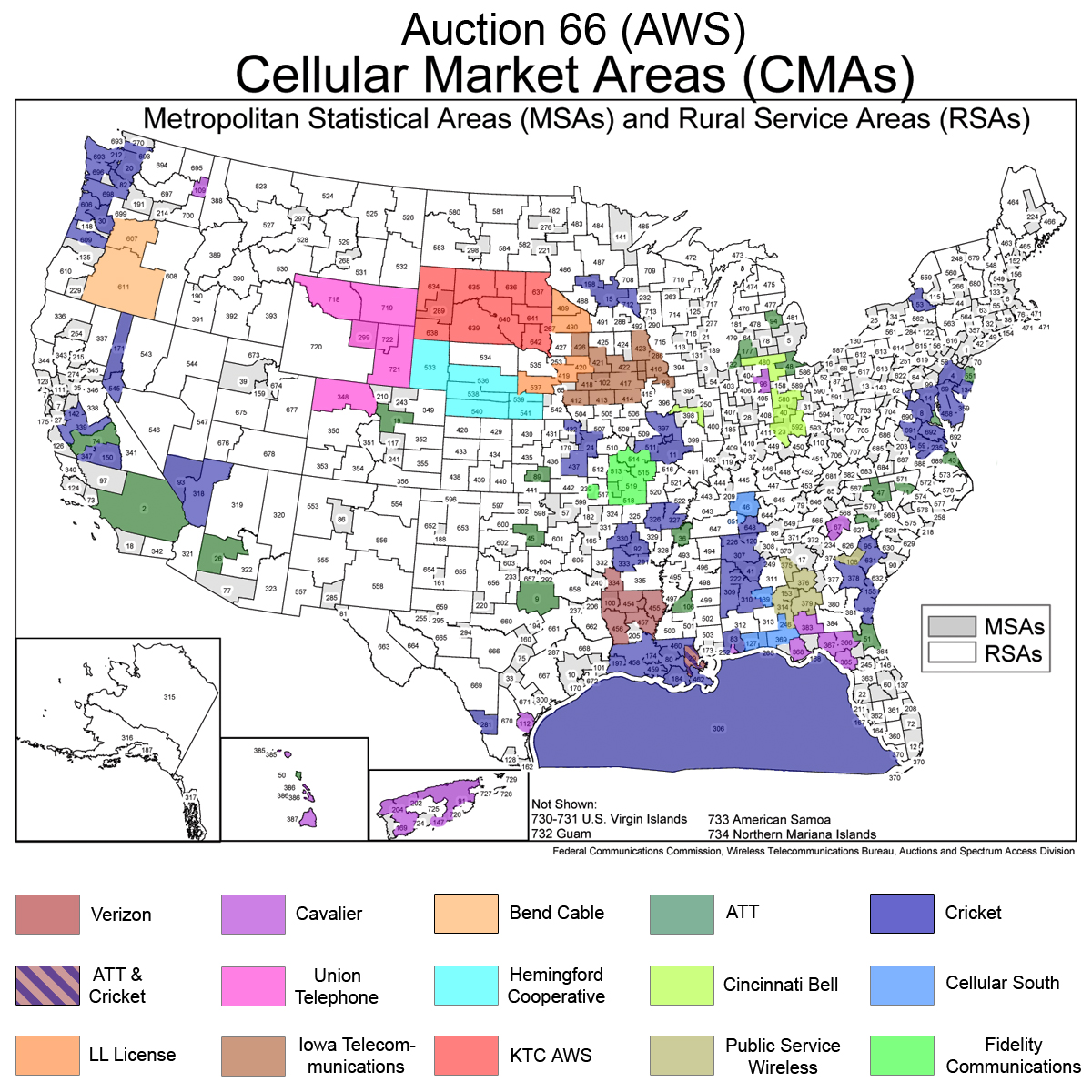

Cellular Market Areas (CMA) Map for Auction 66

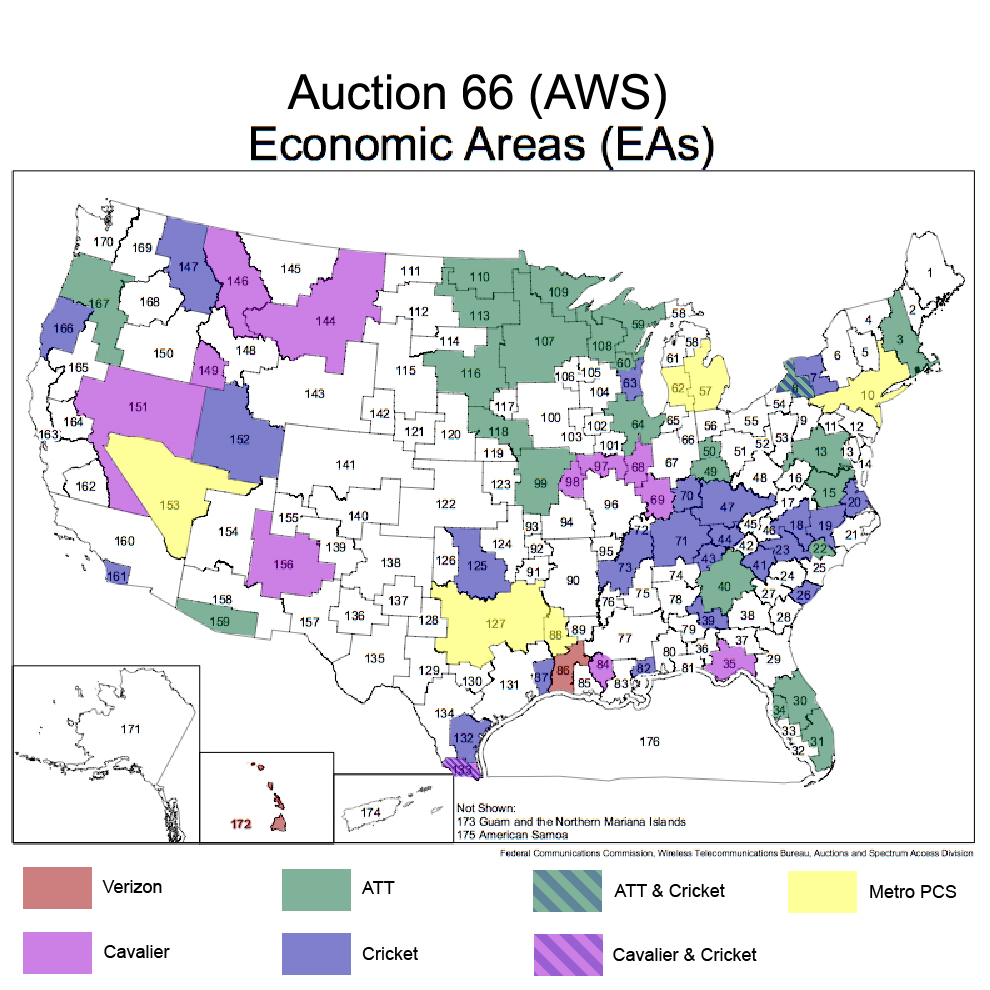

Economic Areas (EA) Map for Auction 66

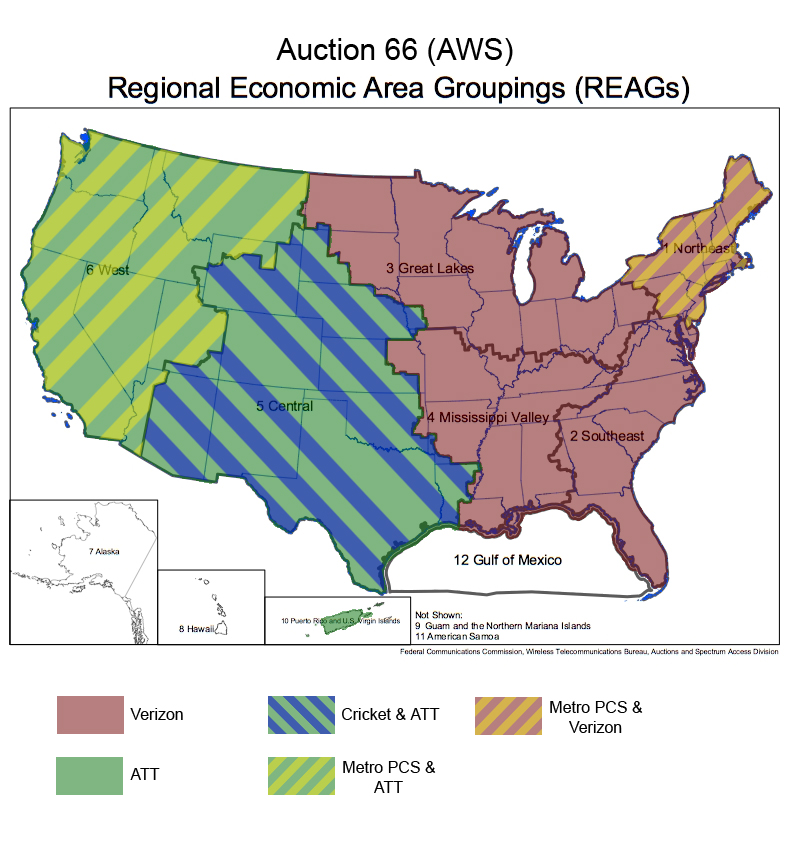

Regional Economic Area Groupings (REAG) Map for Auction 66

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The Big Guys

There are quite a few major actors who qualify as the genuine big guys in Auction 73. Their participation and fundamental interests in this spectrum ensure that the reserve prices will be met and likely exceeded on all blocks (with some caveats on D Block).

QUALCOMM makes the list of the big guys in the auction if for no other reason than it nearly scored national footprint (minus the Western EAG) in a Lower 700 MHz auction. The 700 MHz Band auction provides a source of spectrum entirely compatible with its acquisition for its MediaFLO datacasting enterprise. It may be a C Block contender, but it is more likely that QUALCOMM will concentrate on E Block to flesh out its national footprint and consolidate. This isn’t going to be a QUALCOMM versus the world auction; QUALCOMM will narrowly target specific licenses, go after them tenaciously, and then get out if it looks like the spectrum is going for higher prices than expected.

More below…