I’d like to reiterate what fellow Wetmachiner Harold Feld wrote yesterday: the telecoms incumbents’ claims of problems arising from anonymous bidding are nonsense, part of a campaign to sow disinformation lest Auction 73 (700 MHz) and its success persuade the FCC to permanently adopt anonymous bidding rules for its auctions.

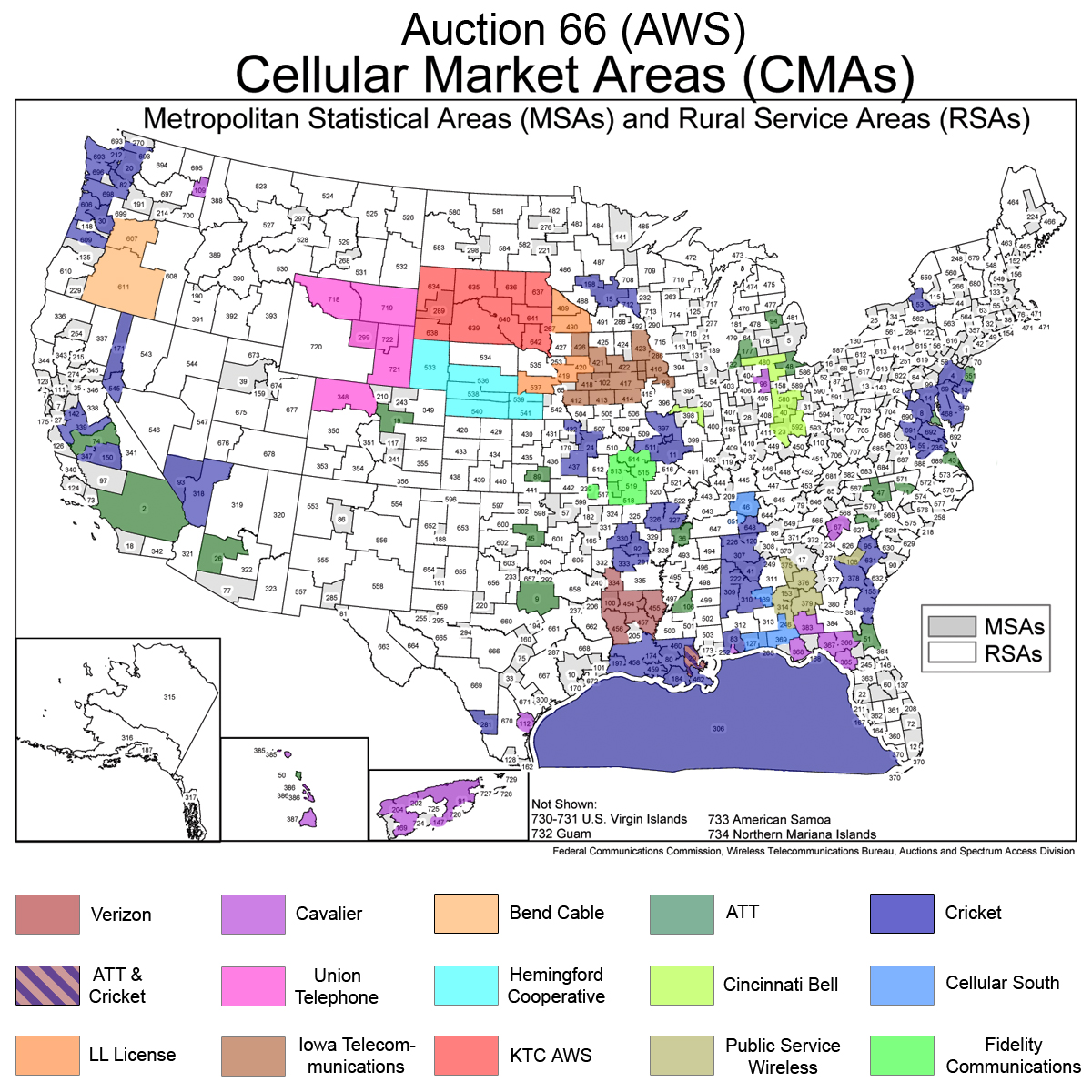

I call your attention to this table, which compares the number of bids on each license in B Block in rounds 1-26 of Auction 73 to the number of bids on each comparable CMA in Auction 66 (AWS-1) in rounds 1-26 of that auction. Note that in general the smaller the CMA number, the larger the population of the CMA (e.g., CMA001 is New York City and its immediate environs, CMA002 is the Los Angeles area, etc.).

What is striking about the data presented in this table is threefold. First, significantly more bids are being placed in general in rounds 1-26 in Auction 73 than in Auction 66. Second, extraordinarily more bids are being placed on the smaller and intermediate-size CMAs in Auction 73 than in Auction 66. Third, a much smaller percentage of licenses are receiving no bids in the first 26 rounds in Auction 73 than in Auction 66.

I am hard put to find an explanation of this extraordinary increase in competition, particularly for the smaller and intermediate-size licenses, which does not involve the effects of anonymous bidding. I suggest that the data, even though they do not disclose bidder identities, are entirely consistent with a more vigorous presence of new entrant and non-incumbent bidders who are protected from retaliatory and blocking bidding by large incumbents by anonymous bidding and are, therefore, more willing to engage in strong competition.

The telcos and cablecos can wail and moan to Communications Daily about the “risks” of anonymous bidding to the FCC, but the principal risk of anonymous bidding seems thus far to be the risk that fat-cat telecoms incumbents won’t be able to get all the spectrum in this auction by their usual bullying and exclusionary tactics. There’s no risk at all to the treasury — revenue from the auction is already wildly exceeding pre-auction projections — and there’s no risk that competition will be wan, as the data presented here amply demonstrate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}