Now we turn our attention to the more experienced potential bidders in Auction 73 for the 700 MHz Band. All have participated in either one or more of the three Lower 700 MHz auctions (44, 49, or 60) or the AWS-1 auction (66).

The Big Guys

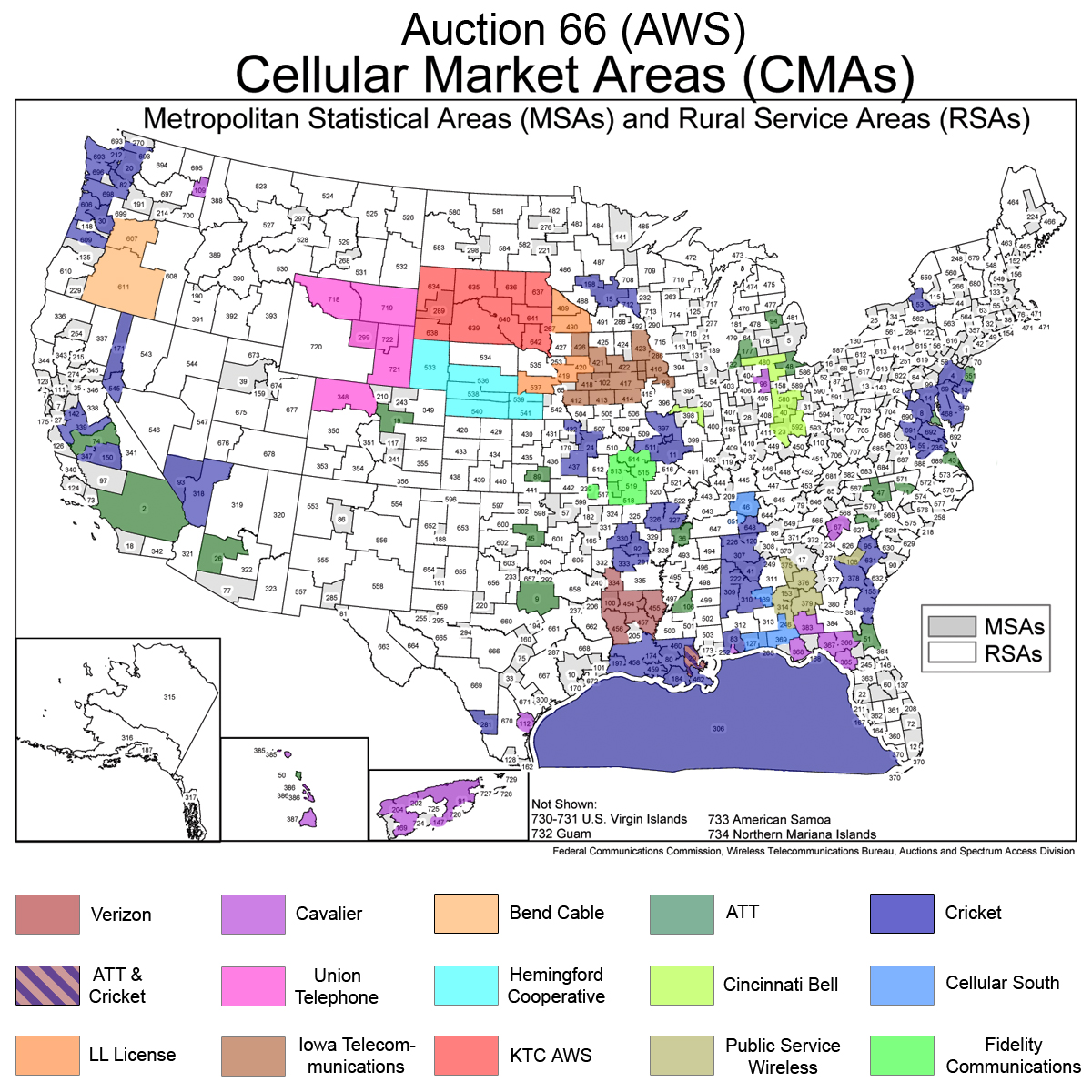

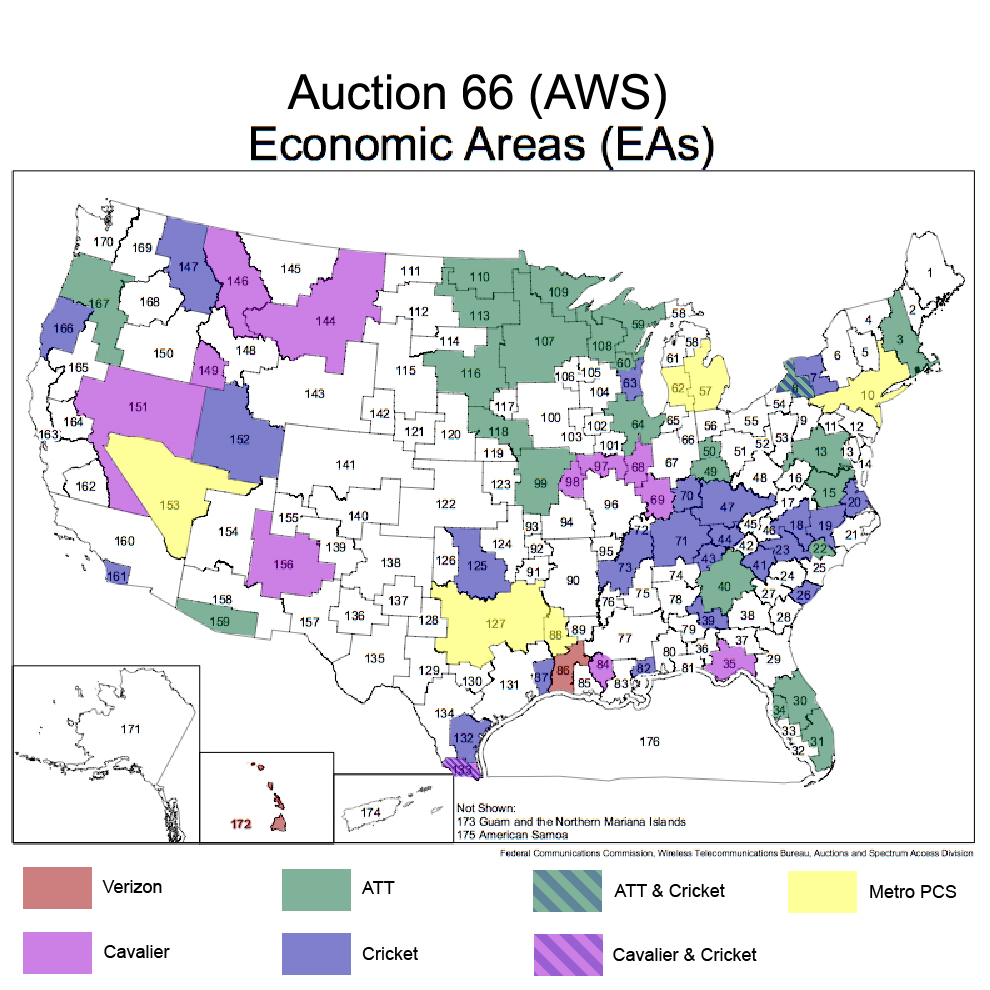

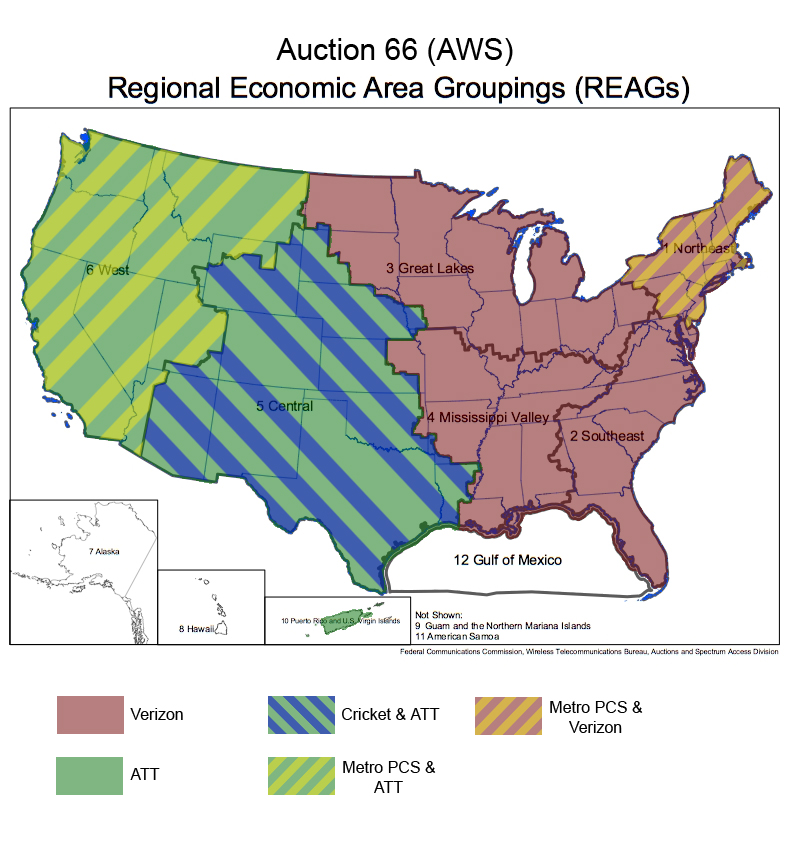

Cellco Partnership, Verizon Wireless’ bidding entity, spent a whopping $2,808,599,000 in the AWS-1 auction for 13 licenses and comes to Auction 73 well positioned to bid for the C Block REAGs and possibly the D Block nationwide license.

MetroPCS 700 MHz, LLC, is the bidding entity for cellular telco MetroPCS, which spent $1,391,410,000 in the AWS-1 auction for 8 licenses. MetroPCS appears to be looking to establish national footprint and will be a strong contender in C Block, and likely using A and B Blocks to fill in coverage gaps.

Cricket Licensee 2007, LLC, spent $710,214,000 for 99 licenses in AWS-1; Denali Spectrum License, LLC, spent $274,083,750 for one license in AWS-1. Both are owned by LEAP Wireless; if their AWS-1 pattern holds, expect them to be mainly active in A and B Blocks, pushing to achieve national footprint, although Cricket may be a C Block contender.

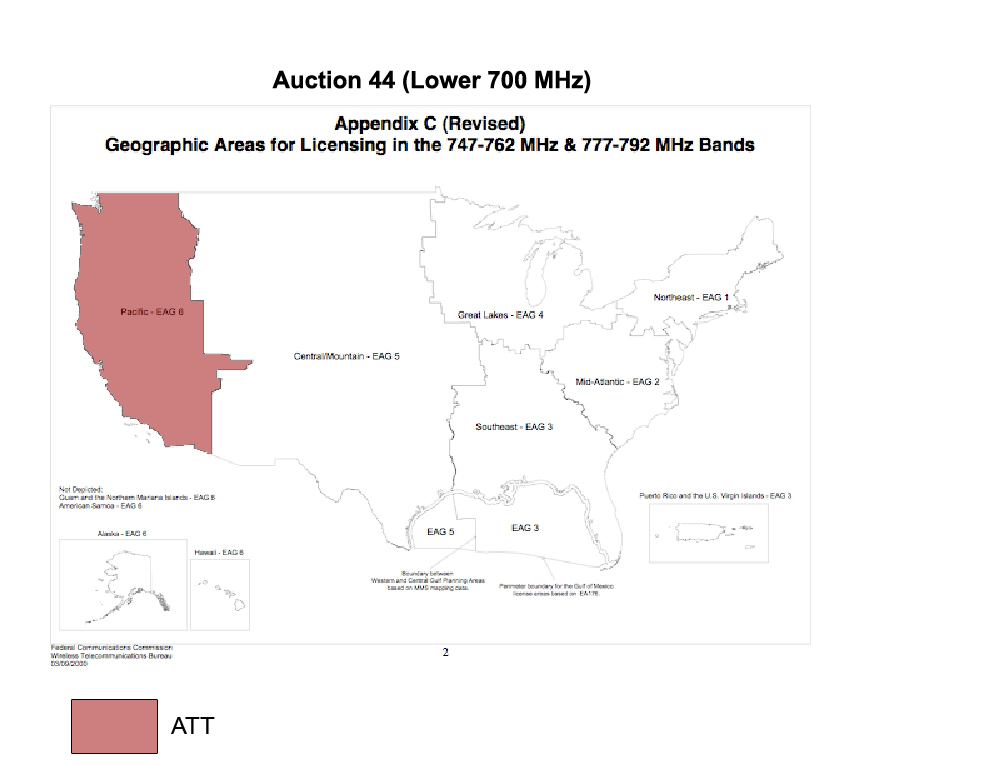

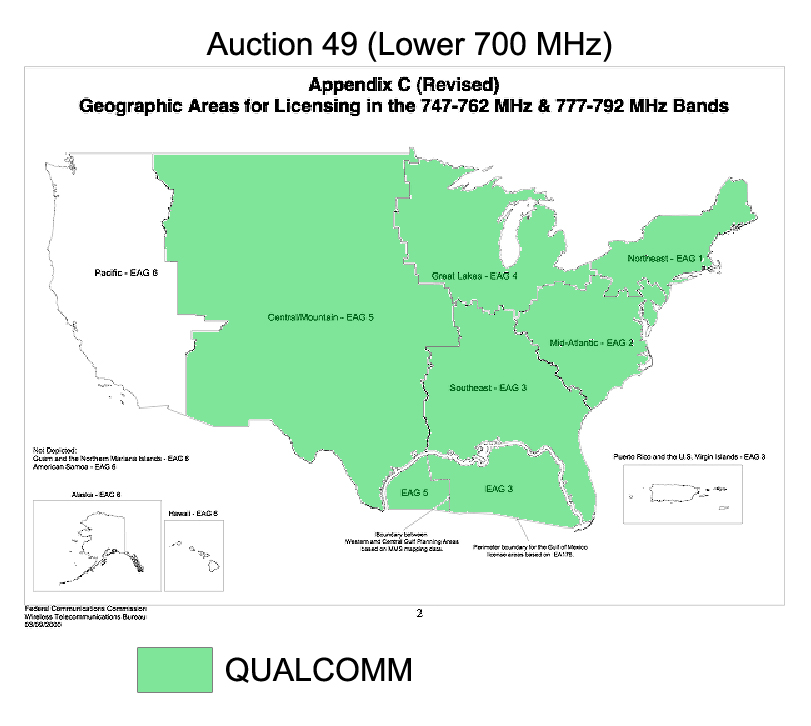

The incredulity expressed by some of the trade press over the application of tech company QUALCOMM,Inc., to participate in the 700 MHz auction seems odd given the fact that QUALCOMM achieved nearly-national footprint in a Lower 700 MHz auction by spending $38,036,000 for five EA licenses. QUALCOMM is positioned to flesh out national footprint in the A and B Blocks or to become a C Block contender.

Cincinnati Bell Wireless, LLC, is the wireless subsidiary of a regional CLEC which spent $37,071,000 for 9 licenses in AWS-1. Expect Cincinnati Bell Wireless to concentrate in the B Block CMAs to reinforce regional coverage.

Bluewater Wireless, L.P., is Aloha Partners’ Charles Townsend’s new stalking horse. Townsend and Aloha Partners spent $34,853,070 in the three Lower 700 MHz auctions amassing the largest bundle of spectrum in the auctions, which they have sold to AT&T for $2.5 billion. Bet on Townsend trying to recapitulate that coup, probably in the A and B Blocks, but Aloha Partners got completely frozen out in the AWS-1 auction, partly by blocking bidding by incumbents, partly because Townsend was unwilling to bid high enough where he wasn’t facing concerted blocking. Auction 73 is shaping up to be more costly than AWS-1, and I doubt that Bluewater Wireless is going to be able to pick up nearly as much spectrum on the cheap as it did in the Lower 700 MHz auctions.

Cellular South Licenses, Inc., the bidding entity for cellular telco Cellular South, spent $33,025,000 for 12 licenses in AWS-1. Look for Cellular South to continue to cover gaps in footprint in the A and B Bocks, although it may compete for some C Block REAGs.

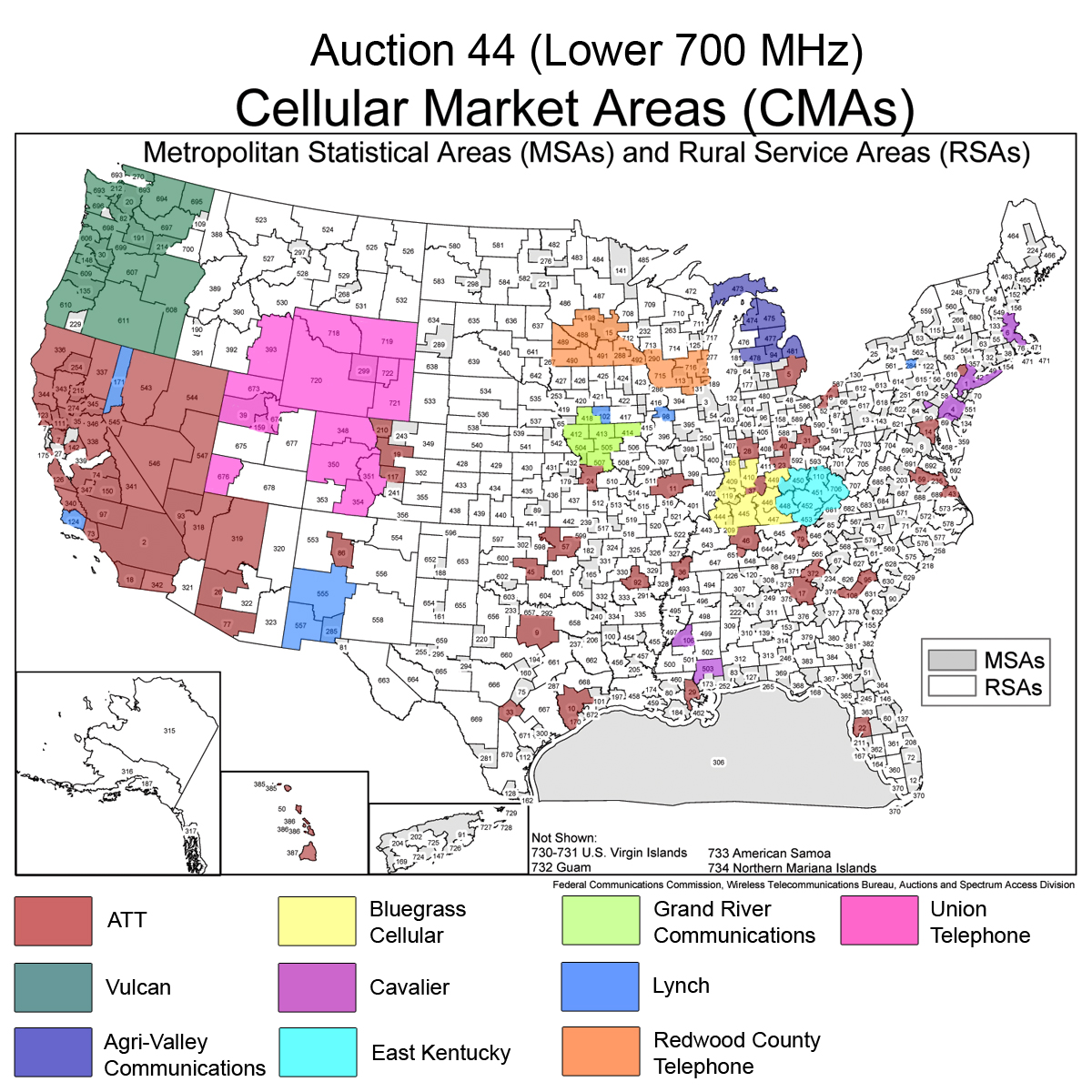

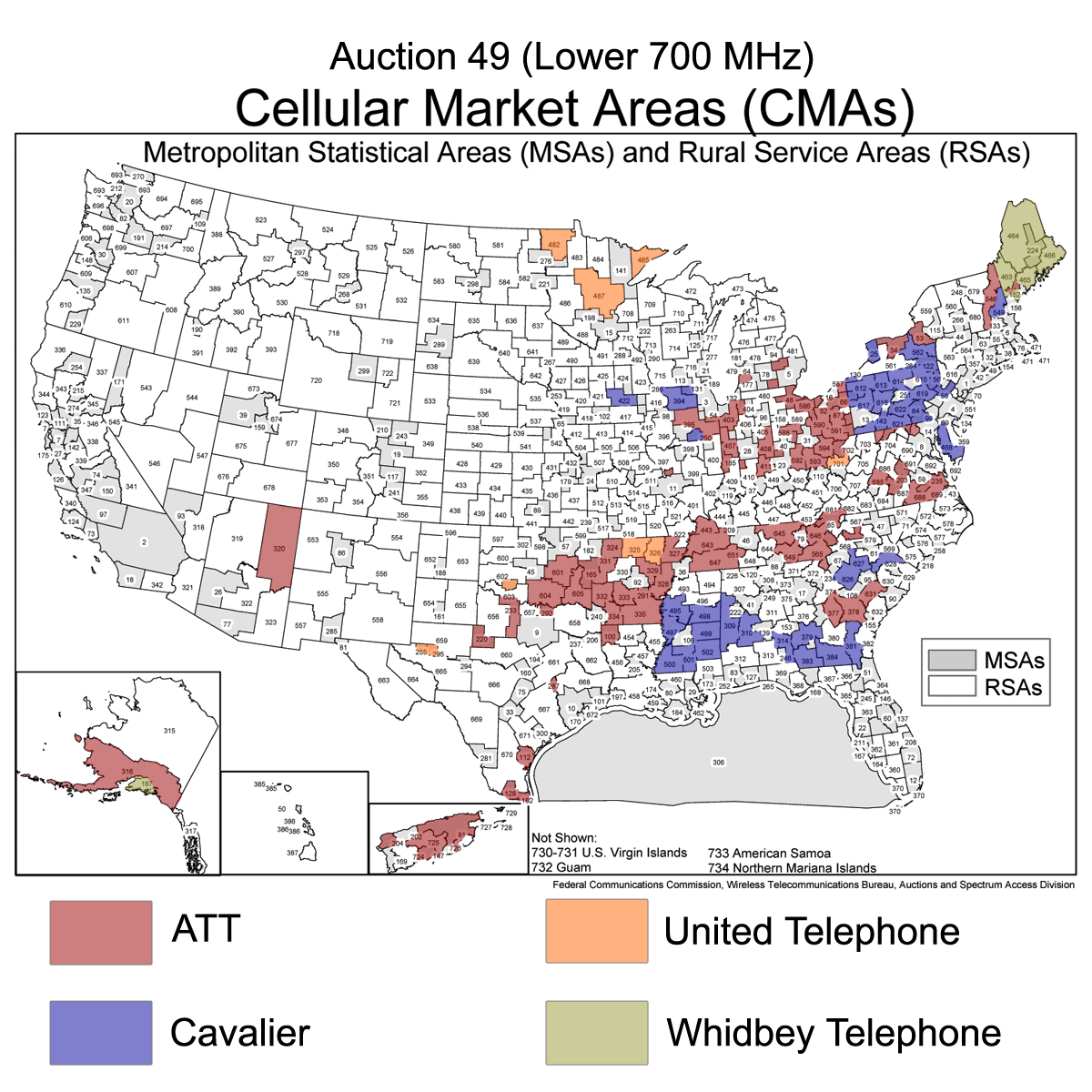

Cavalier Wireless, LLC, spent $23,572,350 amassing 51 licenses in the Lower 700 MHz auctions and 30 licenses in AWS-1. Cavalier may try to establish national footprint or concentrate on firming up its regional dominance.

Vulcan Spectrum, LLC, spent $15,075,000 gaining 24 Lower 700 MHz licenses; Bend Cable Communications, LLC, spent $528,000 on 2 AWS-1 licenses. Both are investments of Microsoft co-founder Paul Allen. They concentrated on obtaining spectrum in the Washington-Oregon region of the Northwest in Lower 700 MHz and AWS-1, but Allen’s deep pockets make Vulcan in particular a potential C Block contender as well as aspiring for regional coverage consolidation in the A and B Blocks.

Cox Wireless, Inc., was part of the SpectrumCo coalition which gained 137 licenses for $2,377,609,000 in AWS-1, as was part of the Advance/Newhouse Partnership. However, the real powerhouses in SpectrumCo — Comcast, Time Warner, and Sprint/Nextel — decided to sit the 700 MHz auction out. However, Cox’s cable TV operations and Advance/Newhouse’s resources as a newspaper, magazine, and cable TV conglomerate position both of them to be significant bidders for the A, B, and C Blocks.

More below…

Continue reading

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}